SynAvia publications and articles

LinkedIn post 03/2021

The German aviation suppliers in the Corona crisis:

Shaping the future in uncertain times - cooperation and strategic partnerships as options for action

Scenario

The Covid 19 crisis has shaken the entire aviation industry. After 15 years of uninterrupted growth, aircraft and engine OEM production rates have dramatically reduced and will not recover from this low level in the medium term. The OEMs and large Tier 1 companies have initiated measures with personnel adjustments, insourcing and the sale of assets that will ensure their survival. In addition, these companies are considered systemically important by their respective governments and receive corresponding financial support.

Particularly affected by the crisis are the SMEs in the downstream supply chain (build-to-print suppliers, commonly known as Tier 3), which are highly dependent on the aviation industry. They have been forced to reduce prices in recent years with cost-cutting initiatives, while being asked to expand their capacity to prepare for production rates of more than 60 aircraft per month. Many of these medium-sized companies have invested in the future ramp-up of production rates and are now often unable to service their loans for the investments they have made and, when short-time working comes to an end, to cover staff costs. However, many of these companies are an important part of the supply chain and represent a high risk for OEMs and system suppliers in the event of insolvency.

There are different assumptions as to when the market will have recovered to the extent that pre-crisis levels will be reached again. The realistic approach is that this will be achieved around 2024 to 2025. In the long term, the civil aviation market will continue to be a growth market.

Consolidation in the aviation industry

Independently of the Covid-19 crisis, a consolidation of companies has been taking place in the aviation industry for some time, from the OEM level (see Airbus/ Bombardier C-Series) to the system suppliers (Tier 1, see acquisitions of Raytheon and Rockwell Collins by United Technologies (UTC), acquisition of Zodiac by Safran Group) and downstream in the supply chain (Tier 2 ... Tier n, see WeAre Group and NextTeam Group in France). The advantage of this consolidation is that it creates

strong and more financially robust companies that cover a broader share of the value chain, take advantage of scaling and low-cost effects, and have the ability to follow their customers on the path to globalisation.

Especially at the international level, i.e. outside Germany, the willingness of companies to merge is very high. Various studies agree that Germany's highly fragmented, predominantly small and medium-sized supply chain has so far been unable to follow this structural change and that this has led to a creeping loss of international competitiveness.

Companies that want to improve their ranking in the supply chain must grow in order to become more important for their customers and to fulfil the important criterion of "financial robustness". Since this is hardly possible through organic growth, there is pressure to consolidate. Companies in the downstream supply chain (Tier 2 ... Tier n) must form larger units through cooperations, JVs or even mergers with large companies in the aviation industry.

Cultural barriers

Self-confident and strong entrepreneurial personalities often find it difficult to get involved in cooperative ventures, since in a cooperation one has to work with partners who want to have a voice and often also a part in the decision-making process. This limits the absolute self-determination that was a decisive motivation for many entrepreneurs when they took the step towards entrepreneurship. It is therefore essential that a cooperation creates a clearly recognisable added value for all cooperation partners involved (win-win situation), which compensates for the disadvantage of losing complete autonomy.

Cooperation with strategic investors

One form of cooperation is the collaboration with a strategic investor. With the selection of the right strategic partner, there is the opportunity, in addition to strengthening the equity base ("financial robustness"), to redefine the business model, to expand the range of products and services along the value chain and thus to advance the diversification of the company and the development of new industries.

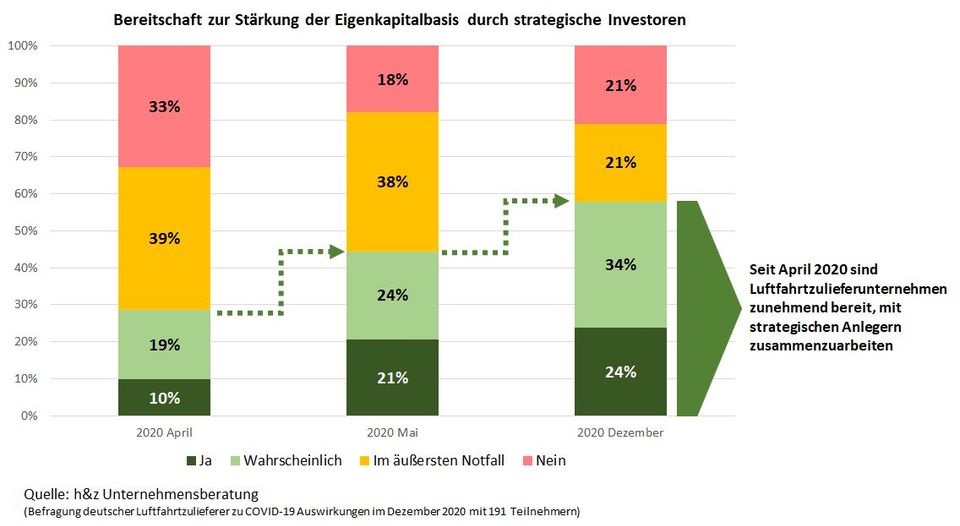

According to a study by h&z Unternehmensberatung, due to the Corona crisis, the willingness of German aerospace suppliers to cooperate with strategic investors has increased significantly over the course of 2020:

Business cooperation is an important strategic option for action

Co-operations and strategic partnerships require the trust of the partners in each other and also in the consulting "co-creators". Experienced, well-connected industry experts are a great help in analysing the market environment and identifying opportunities, risks and dependencies. Derived from this analysis, successful models for strategic orientation, restructuring as well as partnerships that generate added value can be developed.

LinkedIn post 07/2020

Support of French SMEs in the Corona crisis:

Airbus, Dassault, Safran, Thales and the French government support the SMEs of French the aviation supply chain through a concerted action